The US economy hasn’t slowed down. Fourth quarter Gross Domestic Product (GDP) growth was revised slightly from 3.3 percent to 3.2 percent in the second estimate, but predictions for first quarter 2024 growth have increased.

“The increase in real GDP (in Q4) reflected increases in consumer spending, exports, state and local government spending, nonresidential fixed investment, federal government spending, and residential fixed investment that were partly offset by a decrease in private inventory investment. Imports, which are a subtraction in the calculation of GDP, increased,” said the BEA.

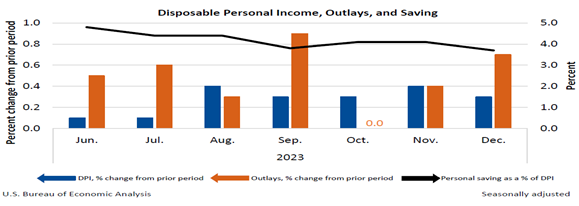

Consumer spending is the main reason growth was so strong. It was revised upward from 2.8 percent to 3 percent annually.

Inflation has been tamed as well. The personal consumption expenditures (PCE) price index increased just 1.8 percent, an upward revision of 0.1 percentage point. Excluding food and energy prices, the PCE price index increased 2.1 percent, an upward revision of 0.1 percentage point.

The PCE price index is the best measure of inflation, since the GDP covers total domestic economic output.

And the Atlanta Federal Reserve’s GDPNow estimate of first quarter 2024 growth was just raised. This has proven to be one of the most accurate future growth predictors, as I’ve been saying.

“The GDPNow model estimate for real GDP growth (seasonally adjusted annual rate) in the first quarter of 2024 is 3.2 percent on February 27, up from 2.9 percent on February 16,” said the Atlanta Fed. “After recent releases from the US Census Bureau and the National Association of Realtors, the nowcast of first-quarter real gross private domestic investment growth increased from 2.5 percent to 4.6 percent.”

Gross domestic private investment is the other driver of growth, as the Inflation Reduction and Infrastructure Act $billions in government spending have seeded the increase in private investments.

And the US economy has been fully employed for more than two years, so there’s a scarcity of workers. Employers have needed to invest more in capital expenditures—whether its AI or more efficient factories—to meet the demand for their products.

This translates to workers being more productive, as I said recently.

Average employee salaries are also higher, and are now rising faster than inflation—as much as 2 percent above inflation in some sectors—which means even more demand for products, thus creating a positive loop. Higher salaried employees spend more, so companies will produce more.

That is why the cost of money has to come down, so companies can finance their projects. I said last week that James Bullard, former St. Louis Fed President, believes Powell’s Fed Governors need to begin to shrink interest rates sooner rather than later.

Bullard, in an interview with MarketWatch’s Greg Robb, said Powell doesn’t want to wait until inflation is actually at the 2% rate. “That would be the ‘Honey I forgot to shrink the policy rate’.” It is a phrase credited to Chairman Powell, who feared that the Fed would react too slowly to the rapidly plunging inflation rate, causing perhaps a recession.

The Fed’s benchmark rate is now in the range of 5.25%-5.5%. The neutral rate is below 4%. There are only three Fed policy meetings before the third quarter of the year. “The math is not adding up that the [interest rate] is going to be at the right level,” said Bullard.

And we have an upcoming budget crunch and possible government shutdown if our political parties can’t agree on next year’s budget in the next couple of weeks! That is the major uncertainty that could inhibit growth this year.

Harlan Green © 2024

Harlan Green on Twitter: https://twitter.com/HarlanGreen