Despite improved builder sentiments, privately‐owned housing starts were down in December at a seasonally adjusted annual rate of 1,382,000. This is 1.4 percent below the revised November estimate of 1,401,000 and is 21.8 percent below the December 2021 rate of 1,768,000.

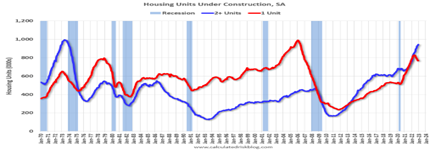

An estimated 1,553,300 housing units were started in 2022 (red line single unit, blue line 2+nnits in above graph). This is 3.0 percent below the 2021 figure of 1,601,000, so housing construction is also in a “swoon”.

And existing-home sales faded for the eleventh straight month to a seasonally adjusted annual rate of 4.02 million. Existing-home sales totaled 5.03 million in 2022, down 17.8 percent from 2021, as last year’s rapidly escalating interest rate environment weighed on the residential real estate market.

“December was another difficult month for buyers, who continue to face limited inventory and high mortgage rates,” said NAR Chief Economist Lawrence Yun. “However, expect sales to pick up again soon since mortgage rates have markedly declined after peaking late last year.”

The 30-year fixed-rate mortgage averaged 6.15 percent as of Jan. 19, according to data released by Freddie Mac on Thursday. That’s down 18 basis points from the previous week — one basis point is equal to one hundredth of a percentage point.

Last week, the 30-year was at 6.33 percent Last year the 30-year was averaging at 3.56%. Rates are now at the lowest level since September 2022.

It is causing a surge in mortgage applications, according to the Mortgage Bankers Association.

The MBA reported its Market Composite Index, a measure of mortgage loan application volume, increased 27.9 percent on a seasonally adjusted basis from one week earlier. The Refinance Index increased 34 percent from the previous week and was 81 percent lower than the same week one year ago. The seasonally adjusted Purchase Index increased 25 percent from one week earlier.

The modest drop in interest rates also helped to end a string of 12 straight monthly declines in builder confidence levels, although sentiment remains in bearish territory as builders continue to grapple with elevated construction costs, building material supply chain disruptions and challenging affordability conditions, per Bill McBride, author of the Calculated Risk blog.

Joel Kan, MBA’s Vice President and Deputy Chief Economist, said “This week’s builder sentiment index from the NAHB reflected an improving outlook and increased buyer traffic, as mortgage rates have backed off from recent highs. The housing market is still in need of more starter and entry-level homes, especially when current demographic trends point to the potential for more younger households to enter homeownership in the near future. New construction of these units will help these buyers entering the housing market.”

Mortgage rates should continue to decline, aided by homebuilders who are now offering initial interest rates as slow a 4 percent to entice buyers. They can do this by buying down a fixed rate and adding its costs to the purchase price, or offering shorter term fixed rates or even an adjustable rate loan.

Will this end the housing “swoon”? There is lots of pent-up demand, and we still have a housing shortage.

Harlan Green © 2023

Follow Harlan Green on Twitter: https://twitter.com/HarlanGreen

No comments:

Post a Comment