Popular Economics Weekly

It’s becoming obvious to me there will be no ‘V’ shaped economic recovery with positive GDP growth resuming in the fall and winter quarters, after the plunges we are seeing in Q1 and projected Q2 growth. The actual Q2 GDP number is not out until the end of July, but economists are saying negative Q2 growth could be somewhere around minus -20 percent.

Why? There are already reversals of business openings as COVID-19 infections soar again in some 35 states. In fact, we won’t really know what GDP growth might be in the fall because the experts don’t know when infection and even death rates will begin to decline again.

That must be why today’s initial jobless claims release shows another 1.3 million jobless claims, same as last week, so new claims for unemployment continue to pour into overwhelmed state employment offices, which means many of the still 15 million unemployed haven’t even begun to receive unemployment insurance more than one month after the $3 trillion CARES Act was passed.

An even better barometer of the jobs market is the continuing claims number, which is 17 million receiving unemployment compensation from the states alone, and with the total of all people receiving benefits through all state and federal programs has hovered near 30 million from the first week of May to late June. These are known as continuing jobless claims. They rose again in the week ended June 20 to 32.9 million.

It is not good news that so many are out of work. The monthly employment report painted a slightly different picture. It showed that the economy regained 7.5 million jobs in May and June, partially recovering some of the more-than 22 million jobs lost during the first two months of the pandemic. A variety of other economic indicators also suggest that more people have gone back to work.

So who really knows what job and economic growth will look like in the fall and winter?

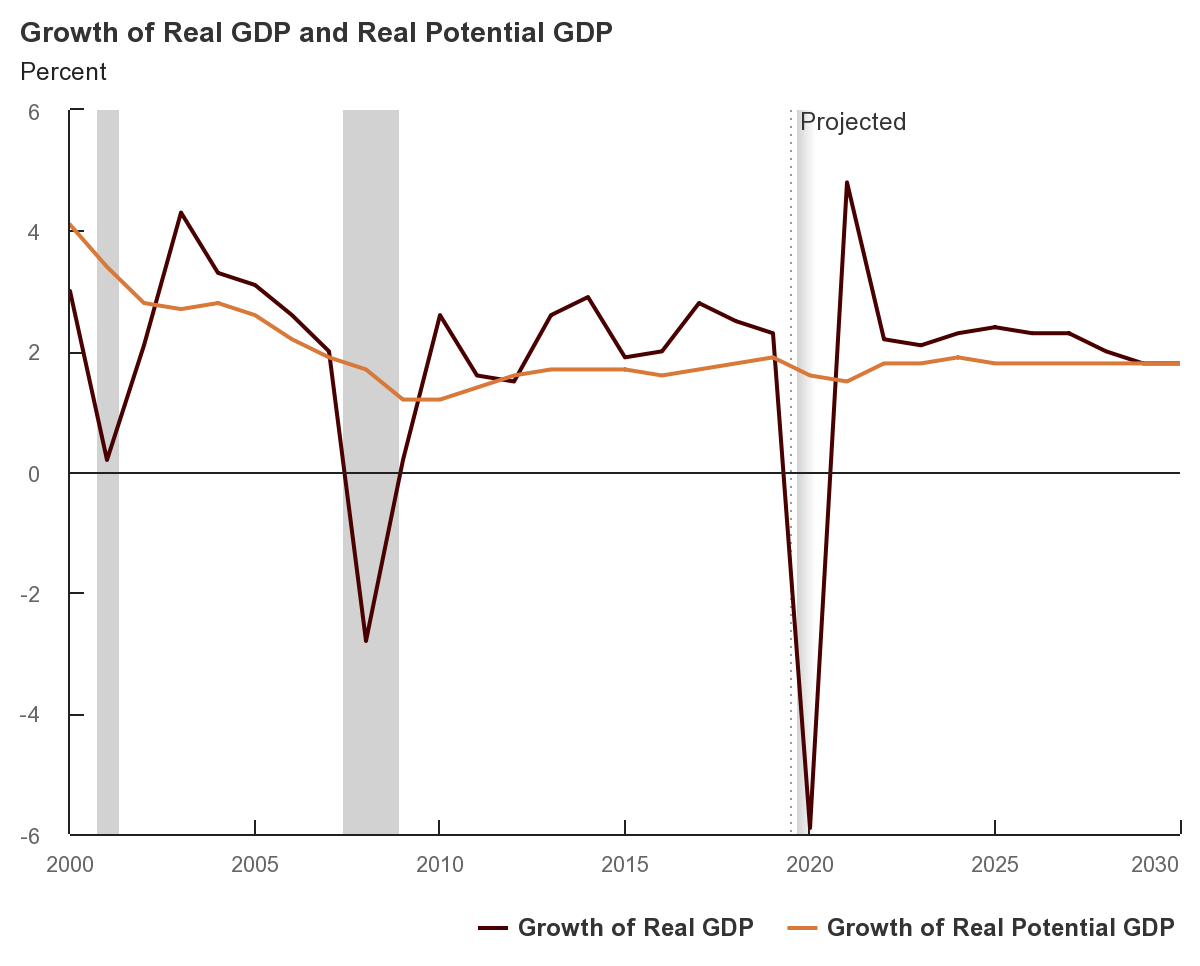

The non-partisan Congressional Budget Office that does projections for congress is also more optimistic in its latest projections. CBO projects that if current laws governing federal taxes and spending generally remain in place, the economy will grow rapidly during the third quarter of this year. So the CBO is saying there could be a ‘V’-shaped recovery!

- · Real (inflation-adjusted) gross domestic product (GDP) is expected to grow at a 12.4 percent annual rate in the second half of 2020 and to recover to its prepandemic level by the middle of 2022.

- · The unemployment rate is projected to peak at over 14 percent in the third quarter of this year and then to fall quickly as output increases in the second half of 2020 and throughout 2021.

“Following that initial rapid recovery,” said the CBO, “the economy continues to expand in CBO’s projections, but it does so at a more moderate rate that is similar to the pace of expansion over the past decade.”They actually mean growth will return to the long-term 2 percent growth rate that has prevailed since the end of the Great Recession, and that won’t happen until at least 2022.

But what about the duration of the pandemic when the US can’t get its united states’ effort together, which the rest of the developed world seems to be doing?

These are not great numbers, unless more ways are found to either boost labor productivity, or US population growth. Our population growth is low because of the declining birth rate and immigration restrictions. Yet neither of them will pick up until this pandemic is really over, and Americans can again come out of their shelters.

Harlan Green © 2020

Follow Harlan Green on Twitter: https://twitter.com/HarlanGreen

No comments:

Post a Comment