One should maybe forgive National Association of Realtor’s chief economist Lawrence Yun’s enthusiasm when he exclaimed “the housing recession is over,” because the NAR’s Pending Home Sales rose for the first time in four months. And this at a time when the Fed’s hit to interest rates had so depressed the housing market, contributing to the severe housing shortage.

"The recovery has not taken place, but the housing recession is over," said NAR Chief Economist Lawrence Yun, "The presence of multiple offers implies that housing demand is not being satisfied due to lack of supply. Homebuilders are ramping up production and hiring workers."

The Pending Home Sales Index (PHSI)* – a forward-looking indicator of home sales based on contract signings – rose 0.3% to 76.8 in June. Year over year, pending transactions fell by 15.6%. An index of 100 is equal to the level of contract activity in 2001, said the NAR press release.

The rest of the US economy has been recovering with second quarter 2023 GDP advance estimate growing 2.4 percent. Interest sensitive real estate sales had been hit hardest with the 5.25 percent in Fed rate hikes, and pending sales gives an picture of sales under contract but not yet closed.

I believe Yun’s remarks may be a sign of something more. A housing market recovery has traditionally been the first indication of an general economic recovery, as indicated by the FRED graph of new-home sales. Existing-home sales follow a similar trajectory. New-home sales have ticked up after every recession (gray bars) since 1960, as viewed in the FRED graph. They are up 23.8 percent annually, to 697,000 units over July 2022, and sales were even higher in June when pro-rated annually.

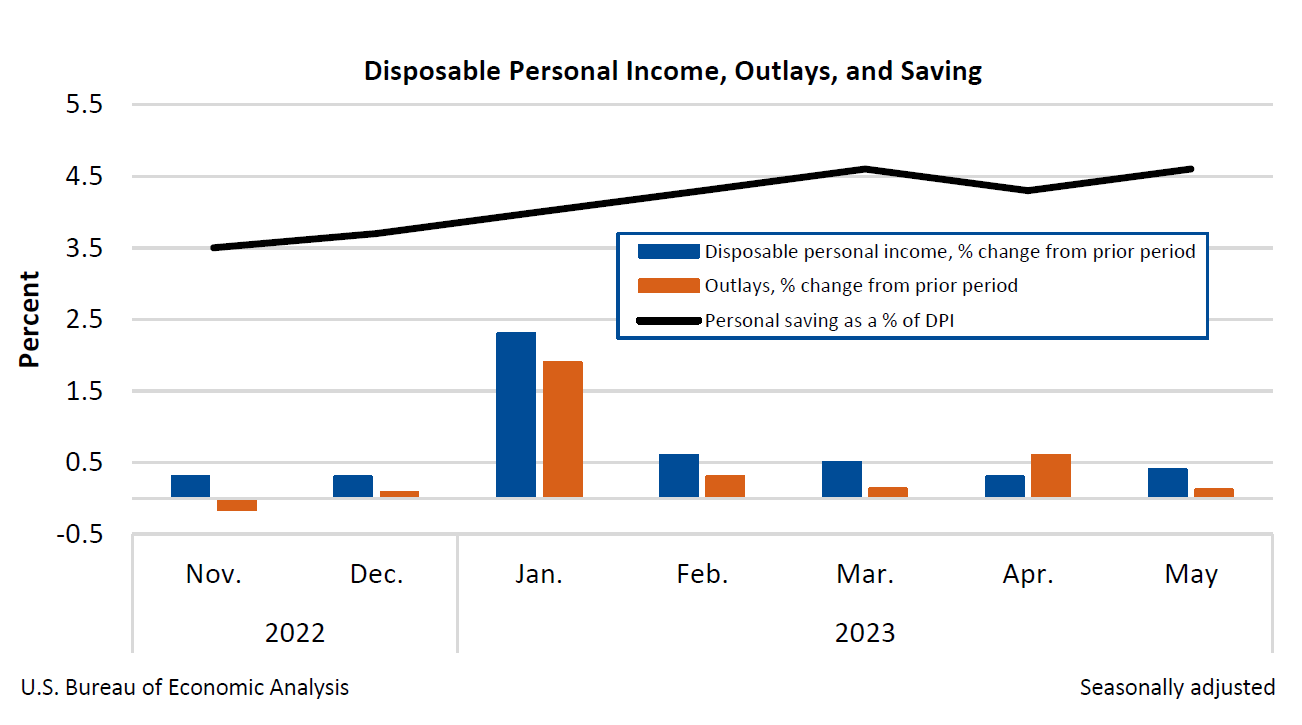

Many other economic indicators are showing recovery in addition to higher Q2 GDP growth, especially consumer spending, which is slowing but gave a boost to second quarter growth.

Even the Federal Reserve has become more optimistic. Federal Reserve Chair Jerome Powell disclosed at Wednesday’s post-FOMC press conference that his staff is no longer forecasting a recession.

“The staff now has a noticeable slowdown in growth starting later this year in the forecast…but, given the resilience of the economy recently, they are no longer forecasting a recession,” Powell told reporters.

Let us hope Yun is right in prognosticating an end to the housing recession, and maybe any recession.

Harlan Green © 2023

Follow Harlan Green on Twitter: https://twitter.com/HarlanGreen

.jpg)

{kind=link}