Answering the Kennedys’ Call

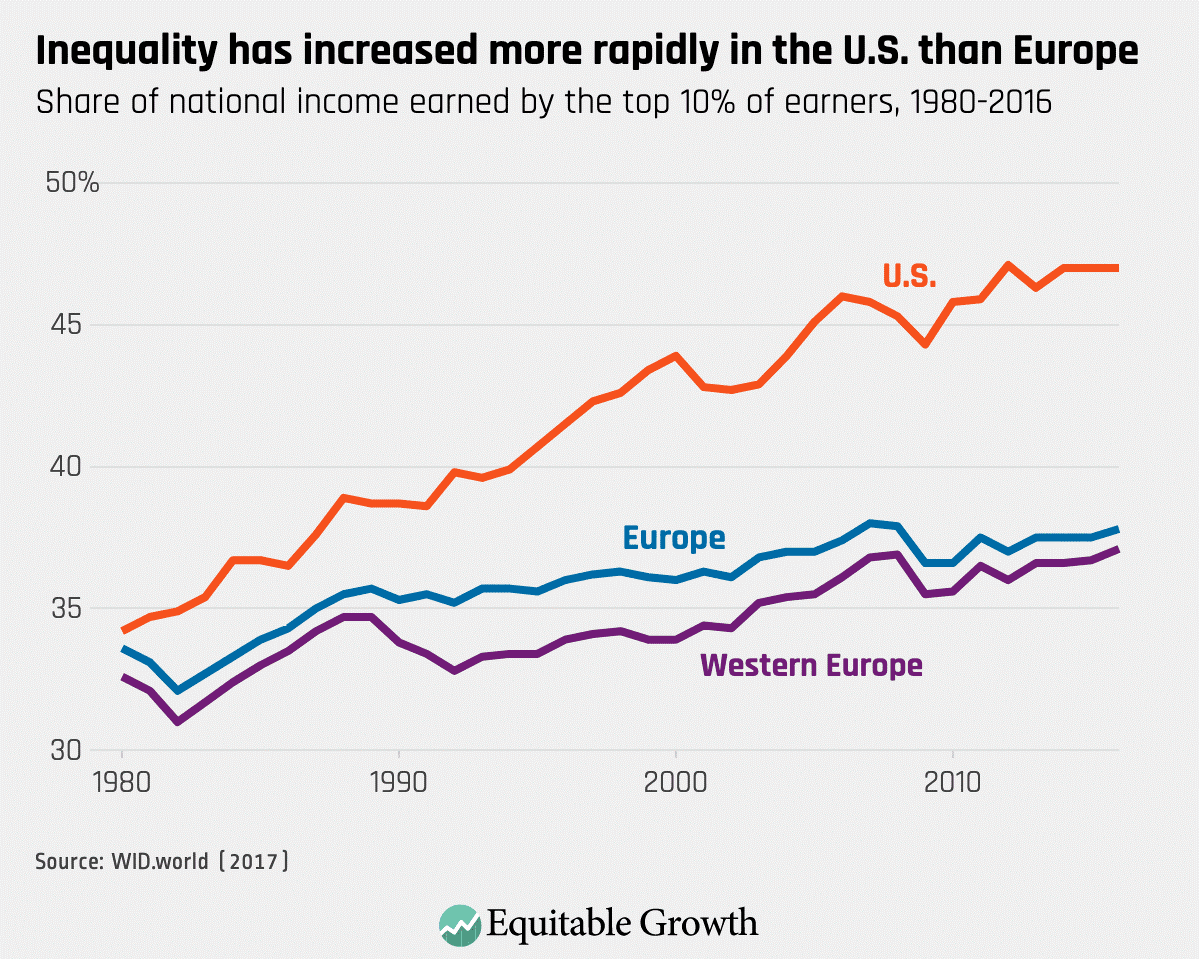

“Every human society must justify its inequalities: unless reasons for them are found, the whole political and social edifice stands in danger of collapse, says economist Thomas Piketty in his latest book, “Capital and Ideology” (Harvard). “War, recession, religion—every facet of human existence has its roots in inequality.”It is a sweeping charge but correcting the record income inequality where the top 10 percent income earners now garner 48 percent of national income will be the only way we achieve a sustainable recovery.

This really means do we want perpetual wars and/or recessions, whether it is due to recurring pandemics, or real wars between the Haves and Have nots?

It has been a long time coming, but the COVID-19 pandemic is the major reason we are witnessing the collapse of a united response and record suffering of Americans with infection and death rates far exceeding that of every other country.

The financial aid to date has focused not on the recovery but First Aid to businesses, with no longer term plan in place to restart the larger economy that has in effect come to a dead halt.

We are a society dependent on consumer spending by ordinary Americans that work in the service sector, which is why it’s bad news that another 4.4 million people filed new jobless claims last week to push the total above 26 million since much of the U.S. economy stopped working more than a month and a half ago.

The spike in unemployment has likely pushed the jobless rate to between 15 and 20 percent, economists estimate per MarketWatch’s Jeffry Bartash. “The only other time in American history when unemployment was that high was in the early stages of the Great Depression almost a century ago,” said Bartash.

The flash services PMI that measure service sector activity fell to 27 from 39.8 in March while the manufacturing PMI dropped to 36.9 from 48.5. Any reading below 50 indicates worsening conditions. It is a preliminary read, with a final read at the end of March but doers anyone doubt it will look better then?

The biggest help to ordinary American consumers that would lead to a sustainable recovery would be reformation of the U.S. health care system, since medical bills are the largest source of private bankruptcies. COVID-19 will probably make a universal health care plan inevitable as most Americans now support it; the question is what its final form will be. There are lots of models as all other developed countries have some private-public version of universal health care for all citizens.

Six-in-ten Americans say it is the federal government’s responsibility to make sure all Americans have health care coverage, including 31 percent who support a “single payer” approach to health insurance, according to a 2018 national survey by Pew Research Center.

Another recent PEW study showed how difficult an economic recovery from the COVID-19 pandemic will be. It has already exacerbated the lack of trust in our body politic between red and blue states, the Haves and Have-nots.

Although there are many reasons for the lack of trust, said the PEW study, a key element is ordinary citizens’ belief that elites are placing their own interests above broader shared values.

“The challenge for the existing political order in affluent countries is to show that it can effectively address problems like poverty and precarity (meaning insecure employment or income),” said a recent New Yorker review of Piketty’s new book. “In America, poverty is increasingly concentrated and thus more corrosive, while absolute economic mobility looks to be at a low point.”COVID-19 is exposing and exploiting the weaknesses of every country that cannot unite behind a common foe. It will make a recovery even more difficult. Need we say more on the distrust engendered by an unlevel economic playing field?

Harlan Green © 2020

Follow Harlan Green on Twitter: https://twitter.com/HarlanGreen

.jpg)