Today’s news that the Consumer Price Index (CPI) was “slightly hotter than expected”, per the Wall Street Journal, caused financial markets to plunge on the assumption the Fed will reduce interest rates more slowly than markets would like to reach its 2 percent inflation target rate.

Yet if we look at past history in the above FRED cpi graph dating from 1950, the only time the Fed reached its target rate of 2 percent inflation for any length of time was right after WWII into the 1960s, and following the Great Recession of 2007-2009 until the COVID pandemic!

So, what does that tell us about monetary policy that is the Feds playing field? It has taken great recessions or WWII (i.e., widest gray bars in graph) to bring down inflation to the Fed’s 2 percent target.

Wow, can acceptable inflation levels only be achieved via recessions? That’s a terrible way to control inflation, in my opinion.

In fact, after 1980 and the Paul Volcker Fed era of sky-high interest rates, the US economy grew very well while averaging 2.5 to 5 percent inflation, until December of 2007 and the start of the Great Recession, which was worldwide let us not forget.

We even had four years of budget surpluses from 1996 to 2000 during the Clinton administration, and the longest period of prosperity (10 years) without a recession.

Yet a few Fed Governors are proving reluctant to accept the fact that inflation is in a prolonged down swing, when today’s ‘slightly hotter’ CPI was almost solely due to sticky used car prices and rental rates.

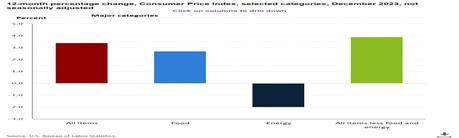

The above official BLS graph explains the ingredients of CPI inflation best. The biggest inflation drop was energy (black bar), along with food (blue bar), though its Core index (green bar) was above the All Items index.

“In December, the Consumer Price Index for All Urban Consumers increased 0.3 percent, seasonally adjusted, and rose 3.4 percent over the last 12 months, not seasonally adjusted.”

What is the real cause of the inflationary surge? Most economists now say it was suddenly interrupted supply-chains caused by the pandemic that returned to normal, thus increasing the supply of things and services, not excessive demand because of suddenly wealthy consumer spending too much due to all the pandemic recovery aid.

Economics Professor James Galbraith, son of New Deal Economist John Kenneth Galbraith said, “There is a wave of reporting to the effect that the Fed deserves credit [for the drop in inflation]. But the fact is that the peak in rising prices occurred in June 2022, and that was only three months after the Fed started raising interest rates.”

Average hourly private sector wages are the main driver of demand-side inflation (via consumer spending) and they peaked in March 2022 at 5.9 percent. Average earnings had already dropped to 5.4 percent in June 2022, continuing their decline to 4.1 percent in December 2023.

So why do Fed Governors keep saying that the unemployment rate must rise to lower inflation? New York Federal Reserve President John Williams, one of the most influential Governors, was cited recently at a White Plains, NY speech per MarketWatch saying U.S. interest rates will likely need to stay high “for some time” until senior central bank officials are confident the rate of inflation is returning to 2 percent. He said the labor market would need to soften a bit more, potentially bumping up the unemployment rate to 4 percent from the current level of 3.7 percent.

We have had the unemployment rate below 4 percent for two years, current 6-month inflation is hovering at 2.5 percent and still declining, and consumers continue in record numbers to travel and enjoy leisure activities, I said recently.

Why spoil the party unnecessarily with another recession?

Harlan Green © 2024

Harlan Green on Twitter: https://twitter.com/HarlanGreen

.jpg)

No comments:

Post a Comment